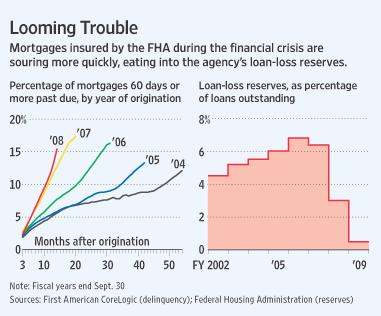

Interesting article... providing perspective on Quantitative Easing

Goodbye QE2 (published 6/27/11) by Preston Howard

|

Preston

Howard |

I’ve been waiting for this day to come. By June 30th, the Federal Reserve will have completed its $600 billion worth of purchases of treasury and mortgage securities and not a moment too soon. The second round of Quantitative Easing (QE2) had mixed results in the broad economy, but negative results on the mortgage market. Accordingly, for those of us who have been waiting for Ben Bernanke to take his hand off of the throttle, the day has finally arrived!

When I state that QE2 has had mixed results, it’s true. We didn’t experience inflation that was so low that it could have led to Japanese-style deflation. The stock market most certainly shot up. In some cases, shareholders recovered 80% of the value they had pre-recession, if not more. That was the good news. The bad news was and is that job growth has been anemic. Only 54,000 jobs (net) were created in the entire nation for the month of May. Not only did the price of oil increase during this time period, but the prices of other commodities increased significantly as well, which severely limited the purchase power of consumers. The first negative effect which was a direct consequence of the announcement of the start of QE2 was its effect on mortgage rates. When the program was launched in November, rates jumped up almost a full percentage point across the board. The refinance market came to a halt and with regards to the purchase market, marginal buyers who barely qualified due to tight ratios no longer qualified. So, as far as a mortgage professional or a buyer with tight ratios or interest rate sensitivities, the demise of QE2 couldn’t come fast enough.

The unfortunate solace to QE2 was all of the bad news that truly brought interest rates back down and not QE2 itself. It wasn’t the first $10 billion dollar tranche, the second or the third tranche that brought rates down; in fact, it’s quite to the contrary. Rates always increased whenever a large purchase of securities was made--from .125% - .25%. In fact, it was the paltry job growth, low payroll figures from ADP, high initial unemployment claims, declines in durable goods, the Euro flu, the fall of Greece, and a drop in consumer confidence which attributed to an improvement in rates. The one lone QE2 announcement that brought rates down was when the Fed confirmed that QE2 would indeed be terminated at the end of June and that there would be no QE3! On that day, mortgage rates actually dropped by .25%. How amazing is that--the announcement of the Fed program’s demise causes the markets to cheer!

So, QE2’s days are truly numbered. It wasn’t all that it was cracked up to be. At the end of the day, the economy has actually slowed down since the second rendition of Quantitative Easing; and Ben Bernanke has admitted such. In a recent interview, he stated that after the Fed has done everything in its power and utilized every tool at its disposal, the job growth still isn’t there and there is nothing else that they can do. He capitulated in stating “we project unemployment to come down very painfully slowly.” The new projection is for growth to accelerate during the fall of next year. For the real estate professional, QE2 was a disaster. Housing sales plummeted, the pending sales index fell, and the total number of homes sold all decreased during the seven-month tenure of QE2. If the program hurts the housing industry, it won’t be good for the rest of the economy. The Fed knows this. At least the program will have ended at the close of business on the 30th and an anemic recovery can get started with participation from the housing industry, leading the way. As I have said it once and will say it again, an economic recovery without a housing recovery is no recovery at all.

Preston Howard is a mortgage broker and Principal of Rose City Realty, Inc. in Pasadena, CA. Specializing in various facets of real estate finance, he can be reached at howardpr@rosecityrealtyinc.com.